The end of the tax year is approaching, and now is an important time to be thinking about your remuneration strategy and tax planning. You will need to consider appropriate levels of salary, pension contributions and dividends, before the end of the tax year on 5 April 2023, and plan for the new one.

Tax bands and your total income in 2022/23

One of the key advantages of working through a company is being able to monitor your total income in the tax year and having the flexibility to retain this within a certain band. It is therefore essential to be aware of the thresholds, so that where possible you can minimise paying tax at higher rates or can retain certain benefits and allowances.

The Government has announced that there will be no increase to the current personal tax thresholds or bands until April 2028. This will mean that more people are likely to fall into higher tax brackets over the next 5 years.

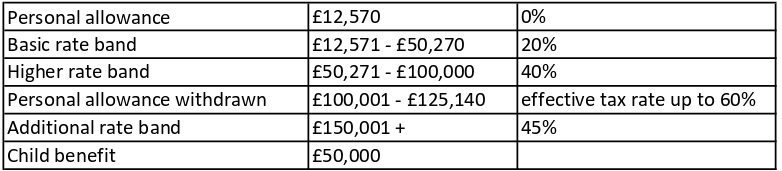

The current bands and tax rates are as follows:

The only band that is changing from April 2023 onwards is the additional rate band. This will be lowered from £150,000 to £125,140, so from 2023/24 any income over £125,140 will be taxed at the additional rate of 45% (this includes dividend income which will be taxed at the highest rate of 39.35%).

Note that it is ‘Adjusted Net Income’ which is the amount considered for the thresholds. This is all your income, including interest, net rental income (after expenses), dividends, pension income (including state pension) LESS personal pension contributions and GiftAid donations. Therefore, you should be mindful of the timing of pension contributions and donations to ensure you utilise them in the most efficient tax year where possible.

When your total income exceeds £100,000, you start to lose your tax-free personal allowance by £1 for every £2 of income above this threshold. The effective tax rate on income that falls within this band can be up to 60%. If your total income is above £125,140, you will lose the whole of the personal allowance.

Anyone in receipt of child benefit (or their partner is) should be aware that clawback of the benefit commences once either partner’s income exceeds £50k. If it exceeds £60k then the whole of the benefit is repayable. Note that the child benefit will continue to be paid in full even if these thresholds have been exceeded, and a tax charge will become due at the end of the tax year, which you are responsible for declaring. The charge applies to the partner with the highest adjusted net income over £50k.

Salary in 2022/23

Have you paid any salary this tax year? If not, consider paying yourself the minimum tax efficient salary of £9,100, which is the level up to which no national insurance (NI) is payable. To qualify for a NI credit for state pension purposes, you need to be in receipt of a salary of £6,396, therefore where possible you may wish to pay yourself at least this level.

If you claim the employment allowance (see below) then a slightly higher salary of £11,908 should be paid.

Once you have paid yourself the minimum salary it is generally more tax efficient to pay yourself dividends because there is no national insurance payable on dividends.

All salary to be included in 2022/23 needs to be reported to HMRC by 5 April 2023. We will be forwarding an email shortly detailing the timetable for making payments prior to the year end. You will need to confirm your salary plans with our Payroll Team so that the correct submissions can be made before the year end deadlines.

If you are in any doubt as to whether IR35 applies to any of your roles, we would recommend that you obtain advice or a contract check from a specialist such as Bauer & Cottrell or Croner Taxwise.

For clients who have worked via their company on contracts deemed to be within IR35, tax and national insurance will, in most cases, have been deducted at source. Please ensure your accountant or the Payroll Team are aware that you have received funds in this way during 2022/23.

Salary in 2023/24

From 2023/24, employees start to pay Employee NI on salary over £12,570, the same as the tax threshold. Therefore, the optimum salary will generally be £12,570 or £1,047.50 per month. Whilst you will be liable to pay some Employer NI, this will be offset by corporation tax savings. If your profits are higher than £50,000, the savings increase due to the extra saving of corporation tax. However, should you prefer not to pay any Employer NI, and assuming you do not qualify for claiming the employment allowance, then a salary of £9,100 would be the level to pay in the new tax year.

Dividends

In 2022/23 the first £2,000 of dividend income is taxable at 0%. We recommend that you take advantage of this allowance, provided you have sufficient distributable reserves available. Please remember that this £2,000 limit includes dividends you receive from any shares and investments you hold, including dividends which are reinvested in new shares, and not just the dividends from your personal service company.

The dividend allowance is being reduced to £1,000 in 2023/24.

If you have no income from other sources, you may wish to fully utilise the 0% bracket of up to £14,570 (personal allowance £12,570 plus dividend allowance £2,000). If you took a salary of, say £9,100 in 2022/23 then you could withdraw dividends of up to £5,470 and pay no tax.

Dividends are treated as the top slice of taxable income. Once the dividend allowance has been used, if your total income does not exceed £50,270, then your dividends will be taxed at 8.75%, which could also be a tax efficient option for you. If your total income is between £50,270 and £150,000, the dividends falling within this band will be taxed at 33.75%. If your total income exceeds £150,000, dividends falling above this threshold will be taxed at 39.35% (threshold changes to £125,140 from 2023/24 onwards).

If your income other than dividends is approaching £100k, any dividend paid (even £2,000) will increase your total income and could mean you lose some of your personal allowance.

As dividends are paid out of taxed profits, you may wish to set aside a cash provision in the company bank account of between 24% and 33% of the dividend paid, to settle future corporation tax (the actual liability will depend on profit level from April 2023).

Any dividend should be paid from the company by 5 April 2023 to fall into the 2022/23 tax year. It is possible to declare a final dividend for the year, and arrange payment on a later date, but this should be formally approved by the shareholders before the end of the tax year.

Salary to spouse or children

Provided you can demonstrate that the family member is genuinely carrying out work for the business, you could consider paying them a small salary. You would need to be clear about the working hours, rate of pay and duties to be performed. Whilst the minimum wage does not apply to children who live with you, this rate nevertheless serves as a good guide for the rate you might wish to pay. For children under 16, you should be mindful that there are the restrictions placed on the number of hours they are allowed to work each week. For employees under 21, no employer NI is payable on salary of up to £50,270, saving a potential 15.05%.

Employment allowance – have you paid Employers NI?

If your company pays at least 2 employees or directors a salary above the secondary threshold, of £9,100 in 2022/23, then you could be entitled to relief for Employers NI of up to £5,000 per year. There are conditions, the main one being that not more than 50% of the work you do should be in the public sector. Please contact our Payroll Team if you would like further details about how to make a claim.

Note that you can backdate a claim for the previous 4 tax years, so if you paid salary to 2 or more people (including yourself) over the last 4 years, and think you paid employers NI but did not make a claim, please get in touch with us.

Pension contributions

Pension contributions paid directly by your company into a personal pension plan are allowable as a deduction for corporation tax purposes, but there are limits. You should consult with an Independent Financial Advisor (IFA) as we are not authorised to give advice on this.

Have you paid yourself trivial benefits this tax year?

This is small allowance but nevertheless one worth utilising. The company can pay for small gifts, for either yourself or someone else, such as wine, clothes, or flowers, and these will be treated as tax-deductible expenses provided certain conditions are met. The VAT may also be recovered if you are VAT registered. For higher rate taxpayers it could save you tax and NI of £171.

You need to make sure you stay within the rules, which for a close company are:

- Maximum of all such benefits per tax year is £300 per director/employee.

- Each benefit must cost no more than £50 (including VAT)

- The benefit must not be cash or exchangeable for cash

- Must not be a reward for services or in any way obligatory.

Short term loans from the company

If you need additional funds towards the end of the tax year, but don’t want your total income to slip into the next tax band, you could consider taking a short loan from the company. This could save you paying tax at a higher rate and may be particularly useful if you anticipate your drawings in the following tax year to be lower.

Provided you do not owe the company more than £10k at any point during the tax year, no benefit in kind will arise. If you take more than £10k you have the option to pay the company interest at a level at least equivalent to the official rate (currently 2%) to avoid any benefit in kind arising. If the loan is repaid within 9 months of the end of the accounting year, no further tax charge will arise.

Any loans taken up to 5 April 2023 which are not repaid within 9 months of the accounting yearend will be taxed at 33.75% (this will be in the form of additional corporation tax).

Capital expenditure

There is currently a temporary super deduction of 130% available on capital expenditure. This is on assets used in the business, such as computers, laptops, and office furniture, which generally qualify for capital allowances. The items must be brand new and purchased between 1 April 2021 and 31 March 2023 to qualify for the new super-deduction (cars are excluded). For an asset cost of £2,000 this will provide an additional tax saving of £114. If you consider that your business will continue to pay corporation tax at 19% (profits below £50,000) then it would be worth considering purchasing any assets before the end of March 2023. However, if your company is expected to make profits exceeding £250,000 next year, then you will likely save more tax by delaying the expenditure and getting corporation tax relief at 25% rather than at the current rate of 19%.

Capital Gains Tax

The annual allowance (the amount on which you pay no capital gains tax) is reducing from £12,300 to £6,000 in 2023/24. Therefore, you may wish to crystallise any large personal capital gains by 5 April 2023. If you were thinking of closing your company, and have reserves of more than £6,000, please contact us to discuss whether it would be beneficial to close now. The maximum potential tax saving from closing your company in 2022/23 rather than in 2023/24 due to this change is £1,260, but the actual saving depends on the percentage shareholding you hold and the applicable rate of tax.

Corporation tax increases from 1 April 2023

Currently companies pay corporation tax at 19% regardless of their size. From 1 April 2023, the rate will depend on level of profits arising in the accounting period. Companies whose profits do not exceed £50k will continue to be taxed at 19%. For companies whose annual profits exceed £250k the tax rate will increase to 25% and those with profits in the range of £50k and £250k will pay a rate of between 19% and 25% (equal to an effective marginal rate on profits arising in this band of 26.5%). The bands of £50,000 and £250,000 limits are reduced accordingly if a company has associated companies or an accounting period of less than 12 months.

If your company accounting year end is 31 March, then planning of things like expenditure is straight forward because profit in the year to 31 March 2023 will be taxed at 19% and then the new rates will apply from 1 April 2023 onwards. For companies with different year ends, the profit will be apportioned on a time basis to create pre- and post-1 April 2023 profit periods, which will be charged at the relevant rates that apply to those. Therefore, in some cases it may be beneficial to consider changing a year end or shortening an accounting period. This could be relevant if you were expecting an unusually high level of income, or making a large investment disposal, prior to 1 April 2023, to avoid the profits being time apportioned and partly charged at a higher rate. Please contact us to discuss if relevant.

Year-end personal tax advice

If you would like specific tax advice relating to your income for the 2022/23 financial year end, please contact us as soon as possible to discuss your requirements.

As you will be aware, our personal tax service is separate from our standard accounting service and is chargeable based on the complexity of the work. We will consider your company planning and level of income, to achieve optimum tax efficiency. Our fee would be agreed with you before carrying out any work. Please be aware that we are not authorised to recommend any financial service products.