VAT Explained

In this guide

- How does VAT work?

- What are the benefits of being registered?

- How do I register?

- When is VAT payable?

- In what circumstances might voluntary registration not be advisable?

- My annual turnover is likely to exceed £85,000, so I need to register for VAT. Which scheme should I choose?

- Can I reclaim VAT on pre-registration expenses?

- What do I need to consider if my clients are outside the UK?

- Are EC sales treated differently to non EC?

- What are the penalties for late payment or submission of a return?

How does VAT work?

One of the first questions that new business owners ask is if they should register their business for VAT. If your turnover in any 12-month period exceeds £85,000, then registration is mandatory. If it is not, you may choose to register voluntarily if you wish. You should consider this option carefully and whether the benefits in your situation are likely to outweigh the administrative cost.

What are the benefits of being registered?

There is an alternative scheme called the Flat Rate Scheme (FRS), which, prior to April 2017, produced an even higher recovery of VAT. However, HMRC introduced a new category for limited cost traders, which means that in most cases, the flat rate scheme no longer produces a better financial return than the standard scheme (although it does still have the advantage of being very simple to operate).

Apart from the financial benefits, being registered for VAT can help promote your business, presenting an image of a large, professional, and well established organisation.

How do I register?

When is VAT payable?

In what circumstances might voluntary registration not be advisable?

If most of your work is carried out outside the UK, then there may be a limited amount of VAT on purchases and expenses incurred in the UK for you to recover. Foreign VAT incurred cannot be recovered through the UK VAT system, although you can make a separate online claim for VAT incurred in EU countries (probably only worth doing if it is significant).

If you are certain your annual turnover will be below £85,000, then you might not want the additional administrative burden of recording all VAT collected and incurred plus filing quarterly returns. There can also be stiff penalties for filing a return late or for filing an incorrect return.

Note that if you choose NOT to register for VAT, you must monitor your turnover on a rolling 12 month basis, and advise us as soon as you think you may exceed £85,000, so we can apply for VAT registration. There are penalties for not doing so within 30 days.

My annual turnover is likely to exceed £85,000, so I need to register for VAT. Which scheme should I choose?

Standard Rate Scheme

Under the Standard Rate Scheme, you charge 20% on your invoices (except if your customer is based outside the UK – in which case please consult with us for further advice). This is VAT that you have collected on behalf of HMRC, which you pay to HMRC at the end of each quarter. You may deduct from this any VAT you have been charged on costs incurred, so the amount you pay to HMRC is usually slightly less than the amount you have collected.

The one drawback of this scheme is that you need to ensure you only deduct the correct amount of VAT. You will need to check each invoice to make sure UK VAT has been charged. In some cases, you will need to provide your VAT registration number to the supplier so that VAT is not charged, for instance to LinkedIn who operate from Ireland (if they add VAT to their invoice you cannot recover it). Therefore, there is a bit of work to do to make sure you get it right.

Flat Rate Scheme (FRS)

HMRC introduced this scheme to make it easier for small businesses to complete their VAT returns. Under FRS, you still charge 20% on your invoices, but do not recover any VAT that you have been charged, other than for some capital assets purchased. It means you do not have to record the VAT you have incurred on purchases and expenses, which saves a lot of extra analysis and there is less chance of ‘getting it wrong’. Instead, you apply a flat percentage of your Gross Sales Income and pay this amount to HMRC, which will be slightly less than what you have collected.

The scheme is only available to businesses who forecast their taxable net turnover not to exceed £150,000 in the subsequent 12 months. Taxable turnover excludes VAT and supplies of services made to businesses outside the UK. Once you have joined, you need to check your level of turnover each year on the anniversary of joining and will usually be required to leave the scheme if this exceeds £230,000 over the previous 12 months.

There is a list of different business sectors, from which you select the most appropriate to you, and each sector has a set percentage to apply to gross sales.

From April 2017, we expect that the majority of our clients are likely to fall within the limited cost trader category, for which the rate is 16.5% (15.5% in first year of registration). A limited cost trader is one who spends very little on qualifying goods which, for consultants, is likely to mean stationery, books and certain software (hard format, not downloaded). Capital items like laptops are excluded as ‘goods’ and all services such as travel and subsistence are also excluded.

HMRC have provided the following further examples of goods that are specifically excluded:

- Accountancy fees, these are services

- Advertising costs, these are services

- An item leased/hired to your business, this counts as services, as ownership will never transfer to your business

- Food and drink for you or your staff, these are excluded goods

- Fuel for a car this is excluded unless operating in the transport sector using your own, or a leased vehicle

- Laptop or mobile phone for use by the business, this is excluded as it is capital expenditure

- Anything provided electronically, for example a downloaded magazine, these are services

- Rent, this is a service

- Software you download, this is a service

- Bespoke software designed specifically for you, this is a service even if it is not

supplied electronically

You will be a limited cost trader if the amount you spend on relevant goods including VAT is either:

- less than 2% of your VAT flat rate turnover

- greater than 2% of your VAT flat rate turnover but less than £1000 per year

If you are not a limited cost trader, you can apply and use the appropriate business category rate rather than 16.5%. This assessment must be carried out on a quarterly basis and the appropriate rate applied each quarter.

You can check the list on the HMRC website to select the most relevant category for your business. As an example, some of the rates are:

- 14% – Management consultancy (including financial consultancy and business consultancy)

- 14.5% – Computer and IT consultancy

- 12.5% – Journalism

If your agreed flat rate is 16.5% and you invoice your client for fees of £10,000 (plus £2,000 VAT), the VAT payable to HMRC will be £12,000 x 16.5% = £1,980.00. This means that you retain £20 of VAT.

In the first year of VAT registration, you are given a 1% discount, so you would apply 15.5% in the first 12 months, increasing the VAT saving to £1,400 on turnover of £100k. This makes the scheme slightly more appealing because it gives you a reasonable retention of VAT in the first year and has the advantage of being easy to apply, making your VAT returns very simple whilst you are getting to grips with everything else. You can switch to the Standard Scheme at any point, and may wish to do so after the first year. You would need to write to HMRC to request this change.

Further information can be found on HMRC in Flat rate VAT notice 733.

Standard Rate vs Flat Rate comparison

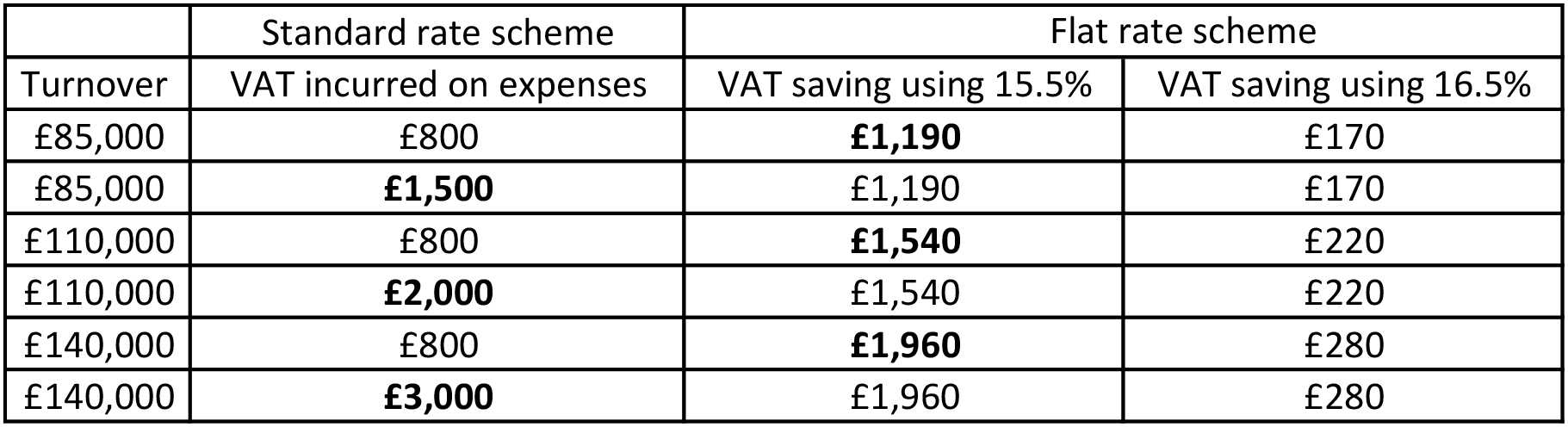

The higher you forecast your turnover to be, the higher the savings to be made from FRS. You should assess the amount of VAT you think you will incur in your first year, and compare this to the savings using FRS. There may of course be situations where the Standard scheme is still best for you, such as if you are going to hire sub-contractors, and therefore you will have a substantial amount of VAT incurred that you will want to recover.

Here are some examples to help illustrate the comparable savings from the two schemes, using different scenarios:

As you can see, once the 16.5% rate needs to be applied after the first year, the standard rate scheme is generally more tax efficient.

For further advice please get in touch. We would be happy to discuss your individual circumstances.

Can I reclaim VAT on pre-registration expenses?

However, you could recover the VAT on a laptop purchased 2 weeks before the business was incorporated or registered for VAT, provided it was purchased specifically for the business. Any VAT recoverable on pre-registration expenses has to be recovered on your first VAT return, and the software we use will work this out for you.

What is Making Tax Digital (MTD)?

What do I need to consider if my clients are outside the UK?

There are a few exceptions to this such as services related to land and property, including architects and surveyors, and some services related to events. In these cases, the place of supply is where the land is or where the event is performed. There are also special rules for telecommunications and digital services.

Are EU sales treated differently to non EU?

What are the penalties for late payment or submission of a return?

For further advice on any aspect of VAT, please contact the team at Competex.