Which VAT Scheme Should I Choose?

My annual turnover is likely to exceed £85,000 so I need to register for VAT. Which scheme should I choose?

Standard rate Scheme

Under the Standard Rate Scheme, you charge 20% on your invoices (except if your customer is based outside the UK – in which case please consult with us for further advice). This is VAT that you have collected on behalf of HMRC, which you pay to HMRC at the end of each quarter. You may deduct from this any VAT you have been charged on costs incurred, so the amount you pay to HMRC is usually slightly less than the amount you have collected.

The one drawback of this scheme is that you need to ensure you only deduct the correct amount of VAT. You will need to check each invoice to make sure UK VAT has been charged. In some cases, you will need to provide your VAT registration number to the supplier so that VAT is not charged, for instance to LinkedIn who operate from Ireland (if they add VAT to their invoice you cannot recover it). Therefore, there is a bit of work to do to make sure you get it right.

Flat Rate Scheme

Under FRS, you still charge 20% on your invoices, but do not recover any VAT that you have been charged, other than for some capital assets purchased. Instead, you pay a percentage of your Gross Sales Income to HMRC, which will be slightly less than what you have collected. HMRC introduced this scheme to make it easier for small businesses to complete their VAT returns. It means you do not have to check every single purchase invoice and there is less chance of ‘getting it wrong’. The scheme is only available to businesses who forecast their taxable net turnover not to exceed £150,000 in the subsequent 12 months. Taxable turnover excludes VAT and supplies of services made to businesses outside the UK.

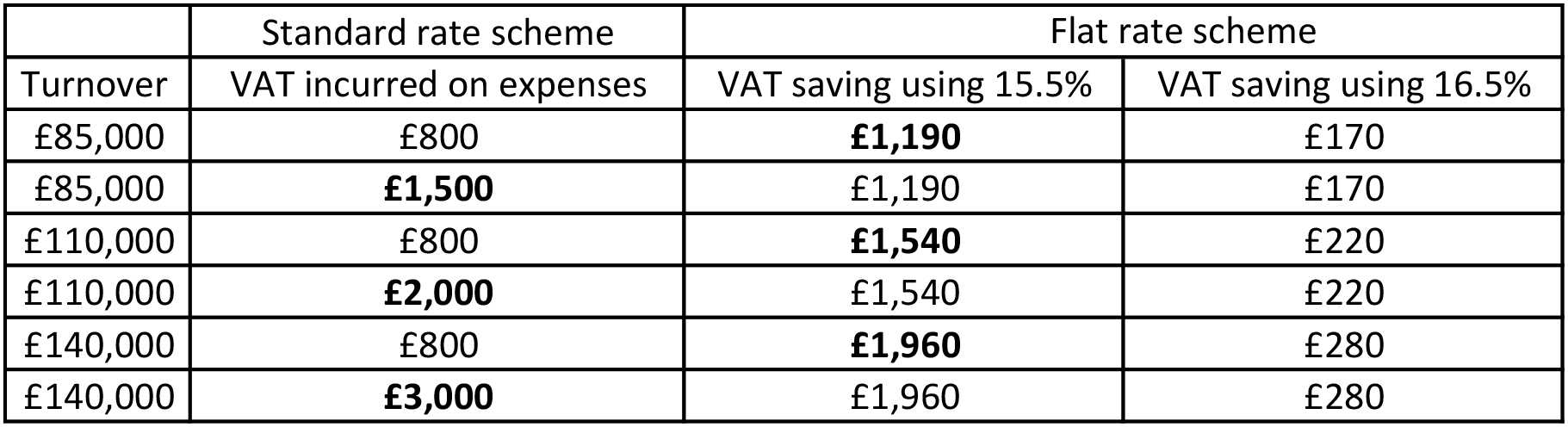

The rate applied to gross sales depends on the business sector most applicable to you, and for most consultants this used to be between 12% and 14%. However, in April 2017, a new category was introduced called the Limited Cost Trader, for which the rate is 16.5%. This category applies to the majority of our clients, because they make limited purchases of relevant goods like stationery and books (capital assets, food and travel are excluded). This means if you opt for FRS, you are more than likely going to have to use the rate of 16.5%, and for a turnover of £100k pa, the VAT you would get to retain would be only £200, making it less financially attractive than the Standard Rate Scheme.

However, in the first year of VAT registration you are given a 1% discount, so you would apply 15.5% in the first 12 months, increasing the VAT saving to £1,400 on turnover of £100k. This makes the scheme slightly more appealing because it gives you a reasonable retention of VAT in the first year and has the advantage of being easy to apply, making your VAT returns very simple whilst you are getting to grips with everything else. You can switch to the Standard Scheme at any point, and may wish to do so after the first year.

The higher you forecast your turnover to be, the higher the savings to be made from FRS. You should assess the amount of VAT you think you will incur in your first year, and compare this to the savings using FRS. There may of course be situations where the Standard scheme is still best for you, such as if you are going to hire sub-contractors, and therefore you will have a substantial amount of VAT incurred that you will want to recover.

Here are some examples to help illustrate the comparable savings from the two schemes, using different scenarios:

Note that with the flat rate scheme, you may still recover VAT incurred on the purchase of capital assets where the invoice value is £2,000 or more including VAT. This is the one exception where you can recover VAT incurred whilst using this scheme.

Whichever scheme you choose, you may also recover VAT on business expenses incurred prior to registering for VAT. Time limits apply, but generally this means expenses incurred up to 6 months prior to registration (sometimes more for capital assets).

For further advice please get in touch with us. We would be happy to discuss your individual circumstances.

Need Assistance?

Speak to Our Team

If you would like to request more information about our services, please get in touch with a friendly member of our team today.