Do you currently incur childcare costs?

If so, you should be aware that employer supported childcare schemes will close to new applicants from 5 October 2018. These include the childcare voucher scheme and directly contracted childcare. Such schemes can save contractors and small businesses a significant amount of tax each year.

However, you can continue getting childcare vouchers if you have joined a scheme and get your first voucher before the scheme closes, as long as you stay with the same employer (continue to be employed by your company).

If childcare is something you currently pay for, it is imperative that you consider your options now to determine whether the existing scheme or the new Government scheme called Tax-Free Childcare (TFC) produce the better savings for you.

If your salary falls within the basic rate band, childcare vouchers can help you to save up to £933 per year, per parent (£2,916 maximum pa @ 32% tax and NI). Higher and additional rate taxpayers could save around £623 a year. In addition your company will receive tax relief on the childcare voucher payments, which will help reduce your Corporation Tax.

In 2018/19 the basic rate band is £34,500 and additional rate band £150,000. At the start of using the scheme, and at the beginning of each tax year, the employer (your company) needs to make an assessment of your basic earnings for that year, which essentially means your forecast salary for the year from the company. HMRC have not specifically mentioned dividends when detailing the basic earnings calculation so it is reasonable to assume that they are not included in the calculation. Please contact us if you require further guidance on this.

Each eligible working parent is entitled to claim vouchers up to a maximum of:

If your spouse also earns a salary from the company then they may also claim vouchers.

If you exceed the above amounts you will need to pay Class 1 national insurance on the excess and will incur a taxable benefit in kind reportable on your P11d at the end of the tax year. Therefore this is best avoided.

Vouchers can be used to pay for any child care provider, childminder, after school club, summer camp, provided they are registered with Ofsted. They can also be saved up, for example to meet childcare costs during school holidays. You would need to keep a record of your eligibility criteria including date of birth of child, details of childcare provider, registration number and expiry date of registration. The scheme must be available to all employees.

If you successfully apply for the new Government Tax-Free Childcare (TFC) scheme you cannot continue to claim childcare vouchers. The new scheme will pay for childcare of up to £10,000 per child each year – so you could get an extra £2,000 per child (up to £4,000 if your child is disabled) each year.

The eligibility and benefits of each scheme differ. Whilst some parents will benefit from the new Tax-Free Childcare scheme, many will be financially better off continuing to use the Childcare Voucher scheme.

Here are the main differences in eligibility:

For more information, and to determine which scheme would be better for you, please go to the Government websites to compare:

Childcare Choices website and Childcare Calculator

In general, parents with more than one child and high childcare costs will be better off using the new scheme as the help increases with the number of children. Childcare Vouchers are better for couples where one parent does not work (in this case you would not be eligible under the new scheme) or if you have only one eligible child and child care costs are relatively low.

If you determine that child care vouchers are the right choice for you then you need to act now to get the scheme in place.

You can either engage one of the providers to administer the scheme for you, such as Kiddivouchers, or just produce the vouchers yourself in the company name (with company logo if you have one).

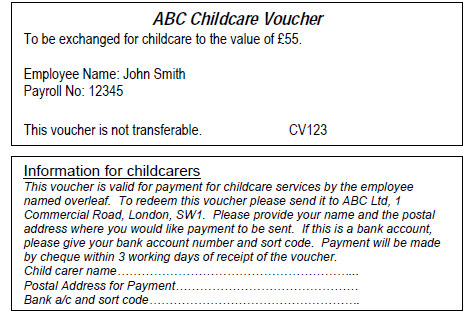

Here is an example of a voucher with the features that HMRC would expect to see:

Note that the company would need to pay the amount to the provider directly from the company bank account.

Alternatively it may be simpler for your company to contract directly with the registered childcare provider. To do this the company should write to the childcare provider informing them that they will pay for part of the childcare costs. The letter provides evidence of the agreement and should state how much they will be paying (up to the maximum tax free amount), date it applies from and the name of both the employee and the child. It should also state that the agreement will end if the employee leaves the employment/ceases to be a director of the company. The childcare provider must provide an invoice for the costs, addressed to the company, and this must be paid directly by the company.

If you would like further information please contact your accountant at Competex.