Financial and other help from the Government: Update October 2020

There have been a number of recent updates on financial and other help available from the Government due to Covid, so we thought it might be useful to provide you with a summary of the things that could be important to you. You may already have read some of the published guidance, so we have kept this as brief as possible and provided links to the more detailed information. Please note that this advice is based on our current understanding. If this should change, following the publication of further detailed guidance (which is promised), we will let you know.

Job Support Scheme

Some of you will have been claiming grants under the current furlough scheme which will be closing on 31 October 2020. The Job Support Scheme will be replacing this and is intended to protect viable jobs in businesses who are facing lower demand over the winter months due to Covid-19. It is not designed for those who are not working any hours at all.

To be eligible you must

- work at least 33% of your usual hours (the Government may increase this after 3 months).

- have paid yourself salary in 2020/21 and reported this to HMRC by 23 September.

For every hour not worked, the Government, and you, will pay a third of your usual hourly salary (the Government contribution is capped at £697.92 a month). Our understanding is that you will not be able to top up your salary above the two-thirds contribution, but we await further clarification on this. You do not have to be working the same pattern each month, but each ‘reduced hour arrangement’ must cover a minimum period of seven days.

Per our previous guidance, for simplicity we will assume that your ‘usual hours’ are 152 hours per month, or 35 hours per week. Therefore, to make a claim you would need to be working a minimum of 51 hours per month or 12 hours per week. In the absence of a contract that confirms your current salary, your ‘usual hourly salary’ will in most cases be the salary earned in 2019/20 divided by 152 hours (we await confirmation of this). If you want to make a claim you will need to pay yourself a salary of at least 77% of your usual salary.

The scheme will run from 1 November 2020 for 6 months. However, it is far less generous than the furlough scheme, under which 60% to 80% of your usual wages could be claimed. The maximum contribution from the Government under the new scheme will be 22%, which you get if you work a third of your usual hours. To claim this, you will be required to pay yourself 55% of your usual salary and will be liable for the tax, employees and employers NI on the whole amount paid to you. This means that the scheme is only likely to benefit employees and directors who are working less than their usual hours but still earning fee income for the company. For directors only, we would not recommend that you apply for the scheme simply to claim the grant, because in most cases the cost of extra tax and NI on the additional salary is likely to be almost as much as, or more than, the grant received from the Government.

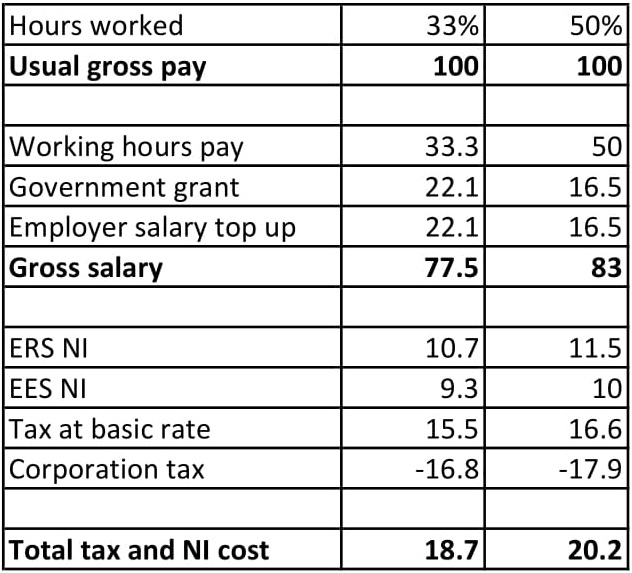

The following illustrates the likely tax and NI costs on the salary that would be paid, compared to the Government grant received. If you are working the minimum level of 33% of your usual hours the cost is £18.7 and the grant is £22.1 per £100 of ‘usual salary’. If you are working 50% of your usual hours the cost is £20.2 and the grant is £16.5.

Assumptions

- Salary paid in 2020/21 to date exceeds £8,788 – ERS NI payable at 13.8%

- Salary falls in the range between £9.5k and £50k – EES NI payable at 12%

- All your personal allowance for the year of £12.5k has already been utilised

- Corporation tax relief – assumes you have taxable profit in your company in this accounting year or the prior one

Obviously the above will vary according to individual circumstances but is intended to demonstrate that this scheme is unlikely to provide a material benefit to the majority. Note that once a minimum salary for the year of £8,788 has been paid it is generally more tax efficient to pay yourself dividends. It might also be more tax efficient to retain the reserves rather than paying further salary.

Large companies are not expected to make any dividend distributions whilst using the scheme. Whether this will also apply to small companies is yet to be confirmed.

If you are working reduced hours (you may currently be claiming under the flexible furlough scheme) then you may wish to apply for the scheme, particularly in the months of November, December and January when you will need to pay yourself a minimum salary anyway to qualify for the Job Retention Bonus (more information below).

Note that the reduced hours you are working would need to be evenly spread over the month. If you work full time in some weeks and then do no work at all in others, you would be unable to claim because you have not worked ‘reduced hours’ in any 7 day period. If you work reduced hours in the first week you can make a claim for this week, but we would assume that you would then have to demonstrate that you have returned to work full time thereafter. Just to repeat, unfortunately the scheme is not designed for those who are working no hours at all.

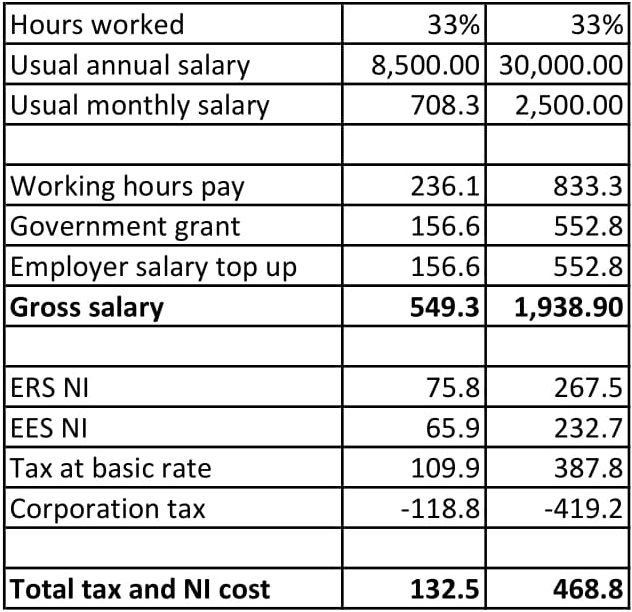

Using the same assumptions outlined above, here are some examples of the possible cost to you of paying more salary compared to the grant that would be provided by the Government:

Note that the grant will be payable in arrears after the payroll return has been filed at HMRC. Competex would be happy to make the claim for you for a fee of £65 plus VAT per monthly claim.

If you wish to make a claim please contact us as soon as possible.

Read the Job Support Scheme factsheet for more information.

Extension of Job Support Scheme for selected companies

Companies who are asked to close as part of local or national restrictions will be able to claim up to 2/3rds of the wages of staff who cannot work – protecting jobs and enabling businesses to reopen quickly once restrictions are lifted. Our understanding is that this will only be applicable to selected companies, mainly in the hospitality sector.

Read the Job Support Scheme for closed businesses factsheet.

Job retention bonus for employers

A one-off bonus of £1,000 can be claimed by employers in February 2021 for every employee who has previously received a grant either under the Coronavirus Job Retention Scheme (CJRS) or under the new Job Support Scheme (JSS). The bonus will be taxable and included in company taxable profits, but there will be no obligation to pay it to yourself as salary (unless of course you wish to).

To be eligible, each employee or director must be paid a gross salary of at least £520 per month on average in November 2020, December 2020 and January 2021 (at least one payment of salary needs to be paid in each of these months rather than one lump sum of £1,560). According to the guidance one salary payment needs to be made during each of the following periods:

- 6 November to 5 December 2020

- 6 December 2020 to 5 January 2021

- 6 January to 5 February 2021

If you think you are eligible then we would recommend you make the minimum salary payments required to receive the bonus. Competex would be happy to make the claim for you as soon as possible after 15 February 2021, for a fee of £50 plus VAT.

Please email Payroll@competex.co.uk to confirm that you want us to make the claim on your behalf and the gross salary you wish to pay each month between November and January – this must be at least £520 on average over the 3 months.

Check here if you can claim the Job Retention Scheme Bonus.

Job Seekers Allowance

Remember if you work less than 16 hours a week you may be able to claim the New Style Jobseeker’s Allowance (JSA) of up to £74.35 per week. You and your partner’s savings and capital are not considered when claiming JSA. However, your earnings and any pension income can affect the amount you receive.

The JSA is a contribution-based benefit. Normally, this means you must have paid or been credited with enough National Insurance contributions in the 2 full tax years before the year you are claiming. You can get JSA for up to 182 days.

HMRC have confirmed that currently you do not need to attend an interview to claim JSA, or go to regular appointments, because of coronavirus.

Read the guidance on Jobseeker’s Allowance.

VAT on hospitality and tourism industry

The lower VAT rate of 5% will now apply until the end of March 2021. If you are VAT registered and using the Standard Scheme you will need to ensure you recover the correct amount of VAT as shown on your invoices for things like hotel accommodation and subsistence.

Bounce back loans

The deadline for new applications has been extended until Monday 30 November.

The loan period has also been extended from six to ten years and there is now the option to make interest-only repayments up to 3 times during the loan period or to suspend repayments altogether for up to six months

Self-assessment payments due 31 January 2021

When your Self-Assessment tax return for the 2019/20 tax year has been filed, you can use the online ‘Time to Pay’ service to set up a direct debit and pay any tax that is owed in monthly instalments over a 12 month period (or shorter if desired).

Eligibility depends on you having

- no outstanding tax returns

- no other tax debts

- no other HMRC payment plans set up

- a Self -Assessment tax bill of between £32 and £30,000

You must set up the plan no later than 60 days after the tax was due, so by 1 April 2021. However, to avoid the risk of penalties you should ensure the plan is set up before 2 March 2021.

If you do not meet these requirements, or need longer than 12 months to pay in full, you may still be able to set up an arrangement by calling the HMRC Self-Assessment payment helpline on 0300 200 3822.

Interest will be applied to any outstanding balance from 1st February 2021.

Time to pay service for all other taxes

HMRC has a new helpline dedicated to providing support to businesses who are unable to pay their taxes on time due to coronavirus 0800 0159 559

Or you can call the Payment Support Service on 0300 200 3835 Monday to Friday, 8am to 4pm

Companies House account filing deadline

Accounts due for filing between 27 June 2020 to 5 April 2021 have an additional 3 months to file their accounts. This means that those with accounting year ends of 31 March 2020 and 30 June 2020, for whom the deadlines would have been 31 December 2020 and 31 March 2021 respectively, the new deadlines will be 31 March 2021 and 30 June 2021.

Different rules apply if your accounting period has been shortened or extended, or if it is your first accounting period.

Competex will continue working within the existing deadlines to ensure you keep up to date, so if you would like more time please contact us to discuss.

We hope you find this useful. If any further information is published which changes the advice contained in here, or if new help packages are announced, we will let you know as soon as possible.