![]()

Provided by ACCA

This is a basic guide, prepared by ACCA’s Technical Advisory team, for members and their colleagues or clients. It’s an introduction only and should not be used as a definitive guide since individual circumstances may vary. Specific advice should be obtained, where necessary.

The headline message from the Chancellor was future tax cuts to support families with the cost of living.

You can read the individual measures below.

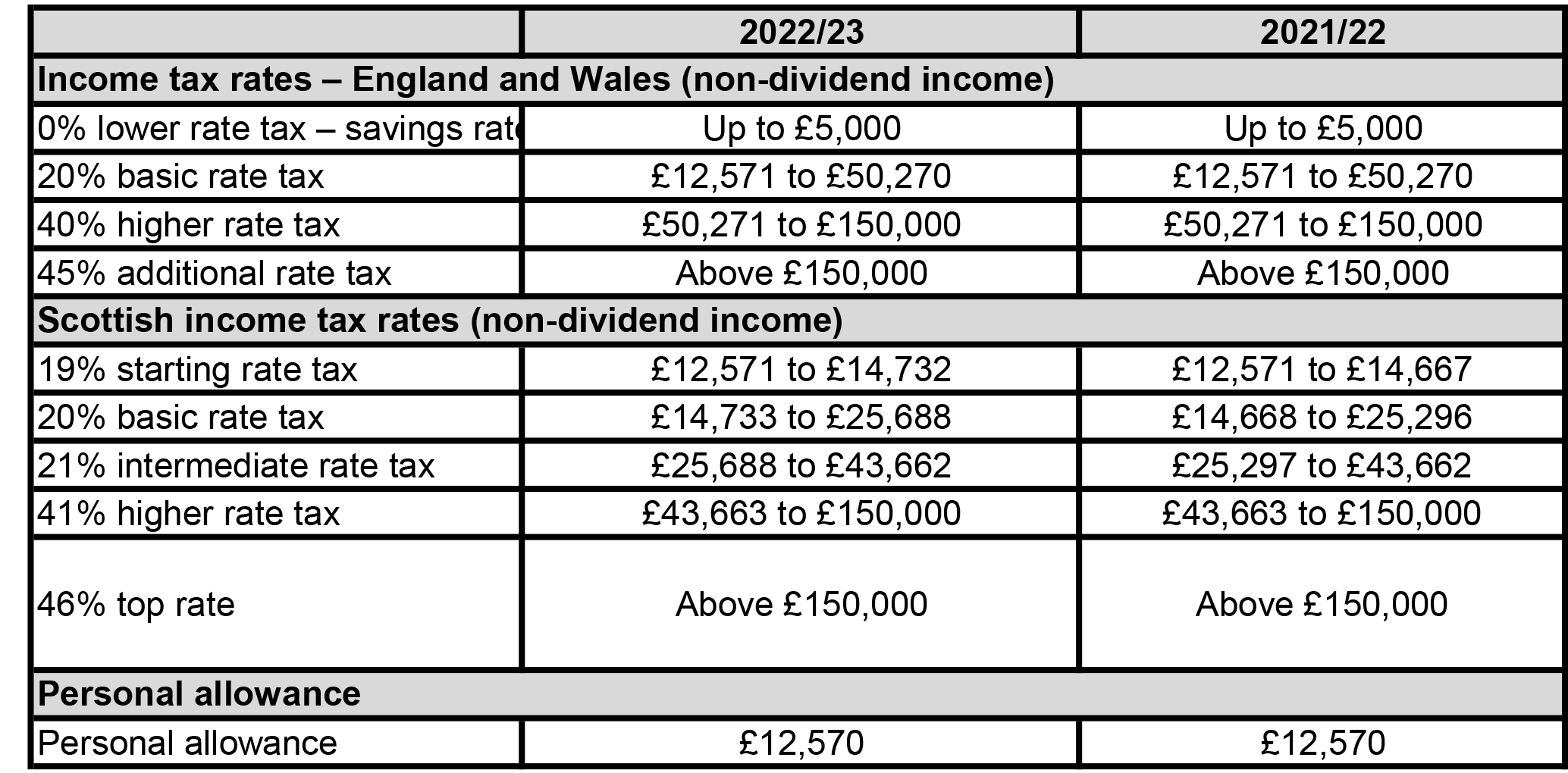

Rates and allowances

The government will reduce the basic rate of income tax to 19% for England and Wales from April 2024.

With inflation at 6.2% and predicted to go higher, the personal allowance and tax thresholds remain frozen. A consequence is that more individuals and businesses are likely to need assistance in navigating the complex tax system.

National Insurance

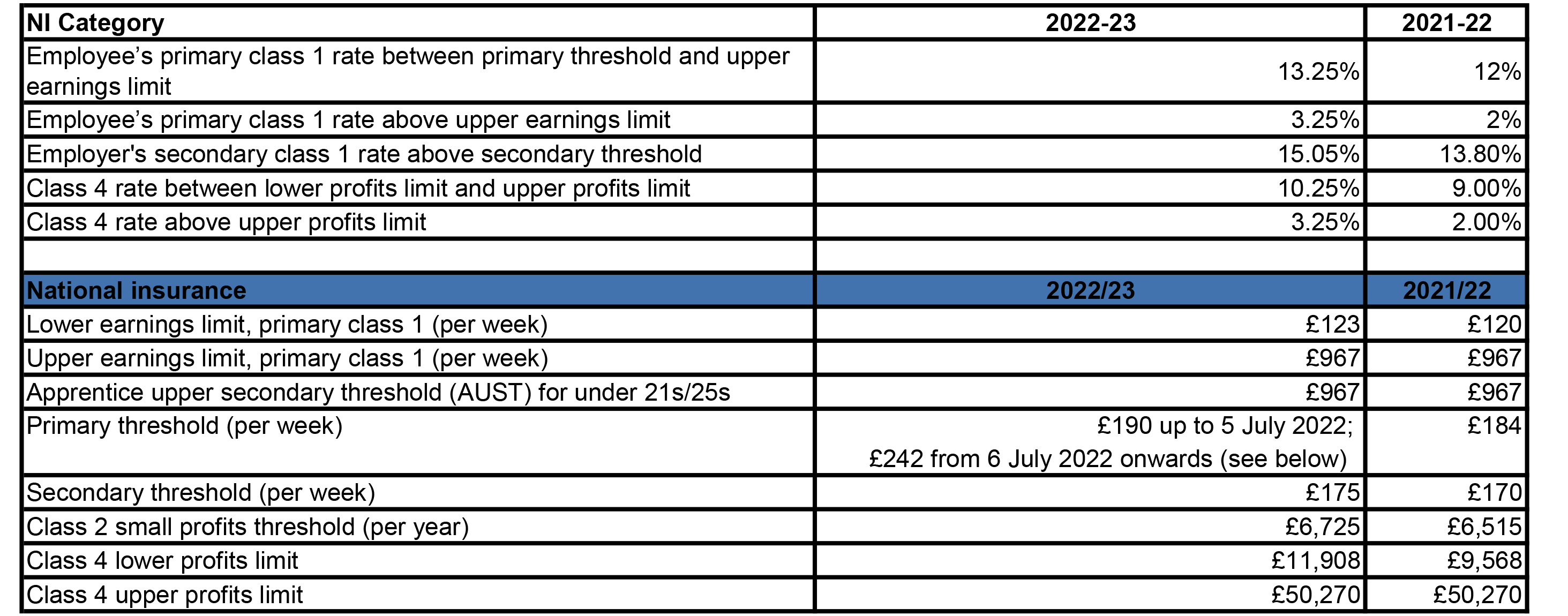

From April 2022 the rate of National Insurance contributions across all classes (except Class 2 and 3) will change for one year. The amount of the contribution will increase by 1.25% which will be spent on the NHS and social care across the UK. This will be replaced by the new Health and Social Care Levy which will take effect from 6 April 2023.

The Chancellor announced that the Primary Threshold and Lower Profits Limit will both increase from £9,880 to £12,570. This aligns the thresholds with the personal allowance.

This increase in National Insurance contributions will apply to:

- Class 1 (paid by employees)

- Class 4 (paid by self-employed)

- Secondary Class 1, 1A and 1B (paid by employers).

Employers will only pay on earnings above the secondary threshold.

The annual National Insurance Primary Threshold and Lower Profits Limit, for employees and the self-employed respectively, will increase from £9,880 to £12,570 from July 2022. July is the earliest date that will allow payroll software developers and employers to update systems and implement changes. From April, self-employed individuals with profits between the Small Profits Threshold and Lower Profits Limit will not pay Class 2 NICs. Over the year as a whole, the Lower Profits Limit, the threshold below which self-employed people do not pay National Insurance, is equivalent to an annualised threshold of £9,880 between April to June, and £12,570 from July 2022.

Employment Allowance

ACCA in representations had suggested an increase in the Employment Allowance. This allowance increases by £1,000 from £4,000 to £5,000. This increase applies from April 2022.The allowance continues to be limited to employers with an employer NIC bill below £100,000 in the previous tax year.

Pensions

With effect from 6 April 2028 the earliest age at which most pension savers can access their pensions without incurring an unauthorised payments tax charge will increase from 55 to 57.

Capital gains tax annual exempt amount (after personal allowance)

These are frozen at £12,300 for individuals and £6,150 for trusts.

Dividend allowance

The tax-free dividend allowance is unchanged at £2,000. The dividend tax rates are increased by 1.25% for each category of taxpayers for 2022/23.

S.455 tax rate on director’s overdrawn loan accounts will also increase from April 2022, from 32.5% to 33.75%.

Corporation tax

The corporation tax rate will remain at 19% but from April 2023 the applicable corporation tax rates will be 19% and 25%. Businesses with profits of £50,000 or below will still only have to pay 19% under the small profits rate.

Enhanced capital allowances: super deduction

Super-deduction allows increased reliefs for expenditure on qualifying plant and machinery incurred from 1 April 2021 up to and including 31 March 2023. Companies can claim in the period of investment:

- a super-deduction providing allowances of 130% on most new plant and machinery investments that ordinarily qualify for 18% main-rate writing-down allowances

- a first-year allowance of 50% on most new plant and machinery investments that ordinarily qualify for 6% special rate writing down allowances

Annual Investment Allowance (AIA)

Annual Investment Allowance is available until 31 March 2023. Businesses will therefore have until March 2023 to consider bringing forward capital investments of between £200,000 and £1m, accessing upfront support by claiming tax relief on such costs in the year of investment.

Recovery Loan Scheme

The Recovery Loan Scheme is extended six months until 30 June 2022 for small and medium sized enterprises and from 1 January 2022 capped at a finance level of £2m per business with the government guarantee reducing to 70%.

Making Tax Digital (MTD)

MTD for ITSA will be introduced from 6 April 2024. This impacts sole traders and landlords, with income over £10,000. General partnerships will not be required to join MTD for ITSA until 6 April 2025.

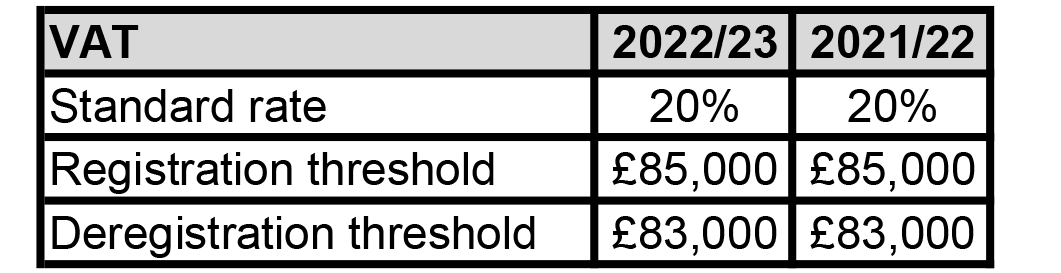

VAT

All VAT-registered businesses must register for MTD.

In July 2020, it was announced that all VAT-registered businesses must file digitally through Making Tax Digital (MTD) from April 2022, regardless of turnover.

HMRC urges VAT-registered businesses to sign up for Making Tax Digital for VAT before 1 April 2022.

The VAT registration and deregistration thresholds will not change for a further period of two years from 1 April 2022.

From 1 April 2022 the VAT rate on energy-saving materials in residential accommodation is reduced to 0% (currently 5%). This measure is introduced until 31 March 2027.

Given the increased costs and inflation we will see many small businesses having to register.

The reduced rate of VAT of 12.5% ends on 31 March 2022 for the hospitality sector returning to the standard rate of VAT of 20% from 1 April 2022.

All VAT-registered businesses must file digitally through Making Tax Digital (MTD) from April 2022, regardless of turnover. HMRC urges VAT-registered businesses to sign up for Making Tax Digital for VAT before 1 April 2022.

Losses

Trading losses will have more flexibility to carry them back over three years. This applies only for losses incurred by companies for accounting periods ending between 1 April 2020 and 31 March 2022, and for individual for trade losses of tax years 2020/21 and 2021/22.

Business assets disposal relief (previously known as Entrepreneurs’ relief)

The lifetime limit on gains eligible for business assets disposal relief is £1m for qualifying disposals.

R&D

SMEs applying for R&D tax credits will be eligible to a maximum of £20,000 in repayments per year plus three times the company’s total PAYE and NIC liability.

Rates

The business rates multiplier will be frozen in 2022/23. Eligible retail, hospitality, and leisure businesses will also benefit from a new temporary 50% Business Rates Relief.

Inheritance tax (IHT)

The nil-rate band remains at £325,000, frozen until 2026. The residence nil-rate band for deaths in the following tax years are:

- £100,000 in 2017/18

- £125,000 in 2018/19

- £150,000 in 2019/20

- £175,000 in 2020/21

- £175,000 in 2021/22 and subsequent tax years to 2026.

Time to pay

Individual taxpayers can set up a payment plan online via GOV.UK by 31 March 2022 to avoid any late-payment penalties.

Pensions

The pension lifetime allowance will remain at its current level of £1,073,100 until April 2026.

Annual Tax on Enveloped Dwellings (ATED)

The ATED charge increases automatically each year in line with inflation (based on the previous September’s Consumer Prices Index).

This is a basic guide prepared by ACCA UK’s Technical Advisory Service for members and their clients. It should not be used as a definitive guide since individual circumstances may vary. Specific advice should be obtained, where necessary.